Treasury Inflation Protected Securities (TIPS) have the properties of a bond. Since bonds are just a kind of loan, we can expect to get our money back when the loan period is over. What makes TIPS especially attractive, however, is that the principal value is adjusted for inflation over time. This eliminates a bond’s worst enemy. This valuable feature does have a drawback, though. There’s more complexity in determining what the value of a TIPS bond is. Not only are there two ways to consider the value as I discuss in the article: Two Ways to Look at TIPS, the value of the principal is constantly changing.

If you’re a saver like me, you are probably interested in the current value of the principal of your TIPS. In order to determine that, we need to adjust the bond’s face value by all of the inflation that has been experienced up to now.

Adjusted Principal

The adjusted principal of a TIPS is the amount of money that you would receive if the bond were due today. You can’t get that money today, but it is the what it would be worth if it were due. For those of us with a strategy to hold the bond until maturity, this is a meaningful number. It gives us a view into how much inflation we have been protected from so far. It is also the number that indicates how much interest you will get on the next coupon. If our coupon (interest) rate is 1%, that 1% is not calculated on the face value of the bond, but on the adjusted principal. That means that your interest is going up with inflation too.

Three Step Overview

It’s actually pretty easy to calculate your TIPS current value. The basic procedure is this:

Get the CUSIP of your TIPS

Go to TreasuryDirect and look up today’s inflation “index ratio” for your specific TIPS.

Multiply the index ratio by the face value of your TIPS.

That’s really all you have to do. If you hold several different TIPS with different CUSIP numbers, you will need to repeat this process for all of your CUSIP’s.

TIPS CUSIP’s

Every bond that is tracked by the public market has a special identifier called a CUSIP. There are thousands and thousands of these but they each identify a single bond issue. When you purchase a TIPS at your brokerage or online you will see your CUSIP for the bond on you “trade confirmation.” For this example we are going to use the current 10 year TIPS CUSIP and that is: 9128283R9. This bond was originally issued on 1/18/2018.

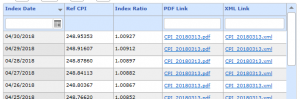

Finding your TIPS Index Ratio

The index ratio for a TIPS is a number that you multiply with the face value of your TIPS in order to determine it’s current real value. TreasuryDirect keeps track of all of these numbers for every TIPS that is currently available on the market. Every day there is a new index ratio for every bond. You can look up the index ratios for your TIPS by going to this page on TreasuryDirect:

When you open this page, you will see all of the CUSIP’s listed for every TIPS that hasn’t matured yet. Then, you click on your CUSIP number. When I click on the number 9128283R9, I get a list dates along with some other numbers in a table. For the sake of my example, lets say that it is April 28th. To get the Index Ratio, I would go down the list to 4/28/2018 and then go over to the Index Ratio column and see the number: 1.00897. You will need to get this number for every TIPS that hold.

Calculating the Adjusted TIPS Value

The last step is easy. For each one of your TIPS that you now have an Index Ratio for, you just take the total face value and multiply it by the Index Ratio. That is your adjusted principal value.

For my example, let’s say that I have two TIPS bonds with the CUSIP 9128283R9 with an original face value of $1000. My total face value for both is $2000. Then multiply that by the Index Ratio I looked up: $2000 x 1.00897. The resulting current value is: $2,017.94. This tells me that my money is currently being protected from $17.94 of inflation.

If I had quite a few different TIPS with many different CUSIP’s, this might take a little while to do. You can make it go a bit faster by getting my free TIPS Tracker Spreadsheet. I hope to make this process much faster when the new software is released.

So, that’s how you do it. It’s pretty neat to see your money go up in value, especially on days when the stock market is down. I urge you to give it a try and experience it for yourself.

It’s important to understand that inflation protection is removed when taxes are applied. Current tax rules disregard inflation, and as a result it’s easy to demonstrate that inflation can cause all of our interest on a TIPS and some of our principle to be lost through taxation alone.

When we consider our inflation adjusted returns, we can easily see that the real tax rate climbs to astronomical levels. This simple example shows how easy it is for taxes to use up all of our real returns.

A Revealing Example

Let’s consider the effects of taxes on our inflation adjusted gains. These adjusted gains are what finance professionals call our “real” gains.

Let’s use the actual TIPS that is being offered as I write this and our current inflation rate. Our current inflation rate is actually 2.2% but we will use 2% make it easier and more conservative. If you buy a $1000, Ten year TIPS with a 0.5% interest rate and experience inflation that averages about 2% during that time, the overall real gain would be 5% over 10 years and the overall inflation adjustment if it stayed the same during that period would be 20%.

After 10 years, your principle would be adjusted to $1,200 and you would have been paid about $60 in interest. The problem is that you are not taxed on the just the $60. The tax rules require that you be taxed on the $60 real gain + the $200 of principle adjustment. If you are paying taxes at a low 15% rate, the rules say that you must pay 15% of $260 or $39. Since you really only earned $60 in real value, you will have paid 65% in taxes.

That’s a very high tax rate for sure, but look what would happen if we had an unusual amount of inflation. This is something we need to consider because our intention is to protect ourselves from both average and unusual changes in inflation.

Let’s change the average inflation to 5%. After 10 years, your adjusted principle would now be $1500 and your 0.5% interest would be $75. Your tax on $575 at 15% would now be $86.25. Since you only really earned $75, taxes will have taken all of your real gain and forced you to take a loss of $11.25 on top of that. That comes out to be a real interest rate of -0.1125% and a real tax rate of 115%.

In a taxable account, the greater the inflation, the less the protection. I can’t honestly say that it provides any protection at all because a taxable account amplifies inflation. It is wrong to assume that our savings is inflation protected just because we hold a TIPS.

One Safe Place

If you open a tax advantaged account such as a 401k or an IRA at a brokerage that allows you to hold TIPS within it, your savings is guaranteed to be protected. That’s because all growth in a tax advantaged account is either not taxable or tax deferred. This means that all inflation adjustments to your TIPS principle will only be taxed once, either before you put it into a Roth IRA or 401k or after you take it out of a traditional IRA or 401k.

The combination of a tax advantaged account and TIPS is currently the only option that I am aware of that will guarantee inflation protection to a person attempting to save money in United States.

I Bonds are Only Guaranteed in Certain Cases

I Bonds are tax advantaged in that they are exempt from state and local taxes. That makes them an even better option than other “safe” investments. This still does not protect them from a total loss of real gains through federal taxation on inflationary gains. There is one more advantage though. If an I Bond is used for tuition, it is tax free and becomes a great way to save for a child’s education.

It is also possible to sell your I bonds at a time in which your taxable income is below your exemption allowance. If your total income falls below the your permitted exemption, then your I Bonds are tax free for that year.

A Problem for All Investments

It’s very important for all investors to understand that this problem exists outside of TIPS and I Bonds. As far as I know, all investments have the potential of losing all of their real gains through taxes that are amplified by inflation. Here’s an explanation of the effects on capital gains:

It’s not just a problem for investors, though. Inflationary gains are taxed in your very own bank account. Your interest may be only $1 per year, and you may have actually lost $5 of purchasing power in your account. You would think that would mean that you lost $4 in purchasing power. Since you pay taxes on your inflationary gain of $1, it pushes the loss even lower than $4. Inflation amplifies your taxation because the more inflation there is, the more tax you pay.

Important Things to Remember about Tax Advantaged Accounts

If you have the ability to have 401k, I highly suggest that you do that. IRAs only allow you to contribute $6,000 per year for those under the age of 50 and $7,000 per year for those over 50. 401k’s allow you to hold far more depending on your income.

If you are a high-income individual. You currently have no guaranteed protection from inflation for savings that I know of. It may be a good idea to consider moving your investments overseas. There are several nations that don’t have capital gains taxes including Mexico and New Zealand.

I got an interest payment from one of my TIPS recently. It feels pretty good to watch your income automatically go up with inflation. As I mentioned in the article: “Introducing Treasury Inflation Protected Securities (TIPS)“, these bonds pay out interest on your inflation adjusted principle. The percentage of interest stays the same, but the bond amount itself goes up as it is adjusted for inflation. That means that your income goes up too.

What I feel when I get my inflation adjusted income, may be a result of the fact that I’m so used to being charged an inflation premium. All I’m really experiencing is consistency. I’m just getting the same purchasing power from my money as I had when I purchased my bond. As I considered the fact that loaning out money is capable of producing an ongoing, inflation protected income, I realized that this could be used to create a reliable income and preserve the principal at the same time.

Considering the Possibilities

I don’t talk very much about the income from TIPS because I primarily focus on their ability to protect our savings, but if you have enough money and don’t want to risk it somewhere else, you could use TIPS as a way of getting inflation adjusted income for the rest of your life while also protecting your principal.

You’re intention would be to preserve the principal for the rest of your life. Perhaps you already have a large sum that is intended for your heirs or for charitable giving in your will. You could be using that money to generate an income while keeping the principle safe and adjusted for inflation.

Even if you don’t really need the income, you could generate it and give it away while you are still alive.

Making Your Own Annuity

There’s really nothing new to creating your own “annuity” with TIPS. It’s just a frame of mind. The only difference is that you are using TIPS for the purpose of generating income. If you do plan to use them in this way, you might consider getting the 30 year TIPS. Not only will the income stay consistent for 30 years, you usually get the highest amount of income from the longer term bonds.

Keeping it Real

You might be wondering why you wouldn’t just use CD’s for this purpose. Remember, that the interest rate for TIPS is a “real” interest rate. That means that inflation has already been calculated into the TIPS interest. You have to subtract the inflation rate from your CD’s current interest rate and then compare it to the TIPS rate.

If, for instance, the interest rate on your CD is 2.04%, and inflation is currently at 1.90%, your real interest rate for the CD is only .14%. If you compare that to a 1% interest rate on a TIPS, you would see that you would earn .86% more “real interest.” That’s a whopping 614% more income on the same principal.

Fee Considerations

There really aren’t any fees when you buy a TIPS, but I like to consider any bond premiums and taxes as fees when you make an annuity out of them.

A premium is when you pay more than the face value for the bond. This happens when you buy a TIPS at auction and the price for the TIPS goes above the TIPS amount itself. It can also happen when you buy a TIPS from someone else on the market. For instance, you may end up buying a $1000 TIPS for $1100 at auction. If you do, you are paying a premium of $100 to get a $1000 TIPS. That $100 is like a fee because you had to pay it up front just to get the bond. It could take a while to recover that fee, but if you are doing it to protect a future income stream from inflation, it may not matter much to you. You are paying for a guarantee, just like you would with insurance. As long as you are still working, you can pay that fee with current income. This is a way of protecting future income while you have current income.

Taxes are a similar kind of thing. With TIPS, taxes are like an annual fee. You could think of it as a fee to the government for using their system to protect your money. The fee is paid at your tax rate. The bad thing about this fee is that it goes up with inflation. That makes this fee pretty expensive in a high inflation environment.

These fees may still be acceptable to you for protecting your income stream. With a commercial annuity, you may end up in the same place when you calculate in the loss of principal to your heirs.

If you were to put this annuity in an IRA or 401k, you would completely remove the tax “fee” and if you were careful to only buy your TIPS at a discount instead of a premium, you would also not have to pay the premium “fee.”

You’re the Boss

The thing that makes this so much better than a commercial annuity, is that you have complete control over the principal. The terms are very clear and your investment is backed by the full credit of the United States. All of the money is still under your control.

If you are wondering why you’ve never heard of this before, it might be because there is no money in this kind of annuity for anyone else but you. When you build your own TIPS annuity, you get to decide what to do with the principal and your heirs get it all back in the end without any exposure to the markets.

Bonds are one of the easiest and most common ways to save money for the long term. There’s a good chance you already own one. If you have a certificate of deposit at your bank or your credit union, you own a kind of a bond. CD’s are quite a bit different than other kinds of bonds, but they have many things in common.

Rather than going over different kinds of bonds, I’d like to explain why they are a good investment for those of us saving for future needs. In a previous article, I described two ways of looking at our investments. Bonds are very useful for the part of our savings that we intend to preserve.

Bonds Eliminate Timing Risk

I mentioned back in my introduction to TIPS that bonds are actually a type of loan. CD’s are loans that you make to the bank. If you ever wondered how to turn the tables on a bank and get them to pay you interest, that’s how. If you have had a CD before, you know that it has an end date. That’s how bonds work. They “mature.” When they do, you get your money back.

Because bonds have a due date, they are great for eliminating timing risk. Bonds come with a promise to return your money on a specific day. If you intend to go on a big vacation in two years, you can get a two year CD at the bank and earn higher interest than you would in a regular savings or checking account. When the CD matures, you get your money back and all the interest right when you need it.

You can imagine what might happen if you put that money in a mutual fund for two years. If you happen to have planned your vacation during the next stock market crash, you probably would have to change your plans. It might be ok to miss your vacation, but putting off your retirement because you took that risk would probably be a bigger deal.

Certificates of Deposit and Inflation

Taking out a two year CD might not be that bad. At the time I write this, CD rates are still quite a bit lower than the rate of inflation. When that is true, you end up paying the bank to hold and protect your money. That’s not always a bad idea. Putting all that money in your house might be worse, but it sure would be nice to be able to keep up with inflation don’t you think?

I Bonds vs. CD’s

You might consider I Bonds for a two year holding time or more. You can’t take your money out for the first year, so if you need the money sooner than that, it wouldn’t be a good idea. If you need the money in less than five years, it would still be a pretty good idea to put your money in an I Bond because it protects your purchasing power at the cost of losing three months of interest. It’s still better than most bank CDs at the time that I write this. After five years of waiting, you can take the money out any time. If you have more than 30 years to wait, you will have to sell your bond in thirty years and get a new one. You can find out more about I Bonds in another article.

The advantage of using an I Bond over a CD is that you are more certain to keep up with inflation. There are CD’s that allow you to “step up” your interest rate if the interest rates go up at some point. The problem with that is that interest rates and inflation are not really linked. The will of the government is in between. Governments occasionally force interest rates lower as a way to “fix” the economy. As a result, CD’s have proven to not be a very precise way to protect your money’s purchasing power.

Using a Bond Ladder

You may have seen an article or heard someone at your bank talk about putting some money in a CD ladder. This arrangement helps you take advantage of changes in interest rates over time. It’s another way to attempt to deal with inflation issues as well.

The idea is that you split up your money, and buy CD’s or bonds with different maturity dates. For instance you might buy one for six months, another for one year and another for two years. The idea being that every six months you would have a CD coming due. When it does, it allows you choose whether you need to use some of the money or put it back into another CD. It also allows you to take advantage of changes in the interest rates as they go up.

When you are trying to save your money for later, bond ladders have much different purpose. When you are using inflation protected bonds like I Bonds or TIPS you don’t really have to worry about the interest rates. Remember that taking advantage of rising interest rates is the kind of thing we do with the part of our money set aside for opportunity investing. When we are dealing with the preservation side, what we concern ourselves with is timing. We just need to ask ourselves: When do I need this money? In this case, we would use a ladder to put the right amount of money in the right place in the future to meet our needs.

Here’s an example. Suppose you need your money in 15 years. It may require that you take out a ten year TIPS, and after 10 years you need to remember to buy another 5 year TIPS when it matures. You can think of your needs like buckets of money. Let’s say that you have one bucket for each year during your retirement. You need a ladder of bonds that reach to each bucket in order to fill them with the right amount of money so that you meet all of your needs.

Beware of Bond Mutual Funds

Bond mutual funds don’t have a maturity date. Shorter duration funds may be safer than stock funds, but they are definitely more risky than just owning the bonds. That’s because the fund share prices change every day based on market forces, not inflation. I plan to explain that more in an article about mutual funds.

A Smart Way to Plan

Bonds are a great way to plan because they are based on time commitments. Not everything in life can be planned, but for things that need to be, it really makes sense to use investments that have commitments built into them so that you can be sure to have money when you need it.

Professor Zvi Bodie of Boston University said something that really shaped my thinking about retirement savings. He said that we should think about retirement savings more like we think about insurance. When I tried that, I realized that it caused me to challenge the advice about retirement that I often hear and read about. It exposed something that I was seeing that I knew didn’t seem right as I was planning for retirement.

Assurances are not Guarantees

Fund managers want you to invest in their products, but they don’t give guarantees. They are careful to have disclaimers so that we understand that we could actually lose our money. That’s worth taking time to consider. Professor Bodie says that these management companies are in a far better position to understand risk management than the common person, yet they refuse to guarantee that you will even have your retirement savings when you need it. They give assurances, but they refuse to give a guarantee. Professor Bodie says that the reason they don’t give a guarantee, is that they can’t. Instead, they leave the risk of the investment with the person who is least knowledgeable about what they are doing.

A good thing to ask ourselves is: “Why can’t they give a guarantee when they are managing the money?” The answer is: “Because the investments they use are risky and they know it.”

Professor Zvi Bodie does a great job of explaining the problem here in his video:

Is it really Savings?

I think that there is terminology that retirement fund salespeople should not be using. They often refer to the money that we put into mutual funds or the stock market and other volatile investments, as our “retirement savings.” In my opinion, the money we are putting into those kinds of investments are actually “retirement ventures.” Since no one is committed to maintaining a specific amount of money in those accounts, I don’t think that it can legitimately be called: “savings.”

When we use the word “savings” we naturally think of money in a piggy bank or money in a banking institution. In those places, our money is insured in some way. Our piggy bank is locked in our house and our bank accounts even have deposit insurance from the federal government. We naturally expect that when we return to our bank, we will find the same amount or more than we left in it, but that’s not how most “retirement savings” accounts work in my experience.

Unfortunately, we need to be on guard when money managers use the term: “savings.”

Guaranteeing our Savings

There are ways to guarantee savings, and some of them come at a cost. We know that insurance has a cost because many of us have insurance for other things like healthcare, our cars or a house. Insurance costs something because someone else is bearing a risk for us. When we think of something as important as our retirement, doesn’t it make sense to insure that it will meet our basic needs? Sure there are things in retirement, like golf or fancy vacations, that we don’t really need. I’m not talking about that necessarily, but what about food and medical needs? What about the power bill or visiting family for Christmas? Do we want to become a burden on our adult children when it can be avoided?

Zvi Bodie brings up an interesting point in another place. He suggests that we consider the fact that we are willing to pay $1000 for fire insurance for our house even though it is very unlikely that our house will burn down. The chances are very small, yet we still pay for it. That’s because we believe that the seriousness of not having a house outweighs the fact that it is unlikely to happen. What good a house if I am unable to live in it in because my retirement savings has disappeared? It doesn’t really make sense to protect the house and not protect my income.

Two Categories of Retirement Funds

Thinking about retirement in this way leads to dividing our retirement funds into two parts. One part is the part you reasonably believe you can’t do without in your old age. The other part is for things that you hope for, but that are not critical to your survival. When we divide it up like this, and get insurance for the critical part, it can lead to peace of mind knowing that our critical retirement needs are guaranteed to be there for us.

Guaranteed Retirement Options

When it comes to ways to guarantee the critical part of your retirement, you might be imagining a large piggy bank or perhaps a bank CD. If you have been reading my blog, however, you know what I think about that. Both piggy banks and CD’s are not usually inflation protected, which means that they are not a guarantee. They fail to be a guarantee because you don’t know what the contents of your piggy bank will buy in 30 years when you need it.

There have been CD’s that were “inflation-linked” in the past but I have not seen any in the last few years. Hopefully, demand for them will increase and they will be offered again in the future.

Social Security

One obvious form of retirement insurance is Social Security. It is inflation protected and it’s definitely something to consider when thinking about your critical retirement savings. Social Security is likely to go through some changes in the future, but I expect that something very similar to it will be available for a long time to come. There’s more about this investment in the article: Possibly the Most Popular Inflation Protected Investment.

Company or Government Pensions

If you happen to have a job that offers a pension that adjusts your payments for inflation, you are in a good position. When I say pension, I mean the old fashioned kind that doesn’t require that you manage the money and that does provide a written guarantee. Pensions that don’t adjust for inflation, are helpful but they don’t guarantee that you won’t run out of money to pay your expenses in the distant future.

Be Careful With Insurance Annuities

Other insurance products are provided by insurance companies by way of inflation adjusted annuities. I would just make sure that the inflation adjustments are connected to actual inflation and not a flat percentage increase each year. It’s important to understand how much you are paying for that insurance up front too. Beware: Insurance companies use the word “guarantee” in a similar way that fund managers use the word “savings.” Make sure you know what they are actually guaranteeing. Guaranteed percentages are not the whole story. You also need to know the exact amount of principal the percentage is calculated against. If the principle goes down with something other than inflation, it’s not much of a guarantee. Also remember that if the guarantee isn’t in writing, it’s still not a guarantee. Insurance companies do and have gone out of business. Zvi Bodie recommends splitting up your funds between companies.

Home Equity

The Equity in our homes really is a form of inflation protection. Because a house is a physical thing that represents one of our important needs, it’s automatically inflation protected. Its value goes up with inflation because a house is still a house no matter what the value of money is. Just having your home paid off is big part of insuring your retirement.

This presents an option for those who have no heirs or have no other choice. Many of us spend our lives paying the bank to own a house. The tables can be turned. It is possible to sell the equity to the bank and have them pay you to live in your own house. That’s what is called a reverse mortgage.

Once again caution is needed. Make sure to read everything in any contract to make sure that the bank isn’t taking too much for themselves in the deal. They may woo you with assurances that the remaining equity will go to your heirs, but I am told that this is often not the case because of high fees. Again, there’s no guarantee.

Another thing to consider is selling your house to your heirs, with permission to continue living in the house as long as you can. Working a deal with your loved ones could be a practical option and it can be a win-win situation with them.

Inflation Protected Bonds

My favorite option is to use Treasury Inflation Protected Securities and I Bonds for savings that I want to insure. I do have to do a bit more work myself, but fees are low or non existent. These are just boring government bonds that usually don’t make a whole lot of interest, but they do one thing very well: they protect long-term savings from inflation and that’s what I’m looking for when it comes to protecting the critical part of my retirement savings.

Further Reading

How to Buy an I Bond

If you are ready to get some I Bonds right now and protect some of your savings, I’ve made some step-by-step instructions to help you set up your Treasury Direct account and purchase your first I bond.

It’s important to understand that inflation protection is removed when taxes are applied. Current tax rules disregard inflation, and as a result it’s easy to demonstrate that inflation can cause all of our interest on a TIPS and some of our principle to be lost through taxation alone.

It’s important to understand that inflation protection is removed when taxes are applied. Current tax rules disregard inflation, and as a result it’s easy to demonstrate that inflation can cause all of our interest on a TIPS and some of our principle to be lost through taxation alone. I got an interest payment from one of my TIPS recently. It feels pretty good to watch your income automatically go up with inflation. As I mentioned in the article: “

I got an interest payment from one of my TIPS recently. It feels pretty good to watch your income automatically go up with inflation. As I mentioned in the article: “ Bonds are one of the easiest and most common ways to save money for the long term. There’s a good chance you already own one. If you have a certificate of deposit at your bank or your credit union, you own a kind of a bond. CD’s are quite a bit different than other kinds of bonds, but they have many things in common.

Bonds are one of the easiest and most common ways to save money for the long term. There’s a good chance you already own one. If you have a certificate of deposit at your bank or your credit union, you own a kind of a bond. CD’s are quite a bit different than other kinds of bonds, but they have many things in common. You may have seen an article or heard someone at your bank talk about putting some money in a CD ladder. This arrangement helps you take advantage of changes in interest rates over time. It’s another way to attempt to deal with inflation issues as well.

You may have seen an article or heard someone at your bank talk about putting some money in a CD ladder. This arrangement helps you take advantage of changes in interest rates over time. It’s another way to attempt to deal with inflation issues as well.